Introduction:

If you’re in the market for a new home or looking to refinance your current mortgage, you may have heard the term “conforming loan limits” being thrown around. But what exactly are conforming loan limits, and how do they affect your ability to obtain a mortgage?

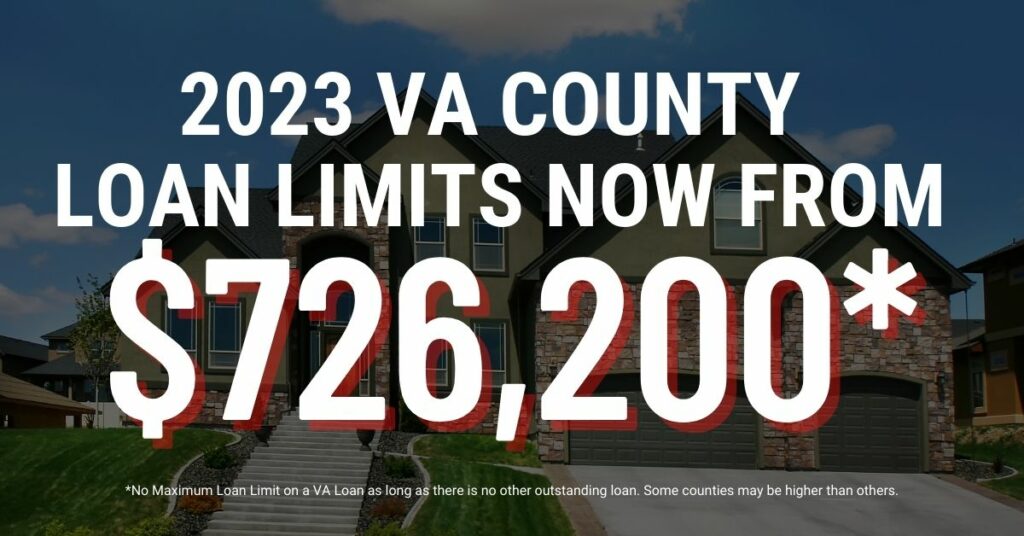

In this article, we will discuss everything you need to know about conforming loan limits for 2023. From what they are to how they are determined, we’ve got you covered. It’s important to note that for 2023, the conforming loan limits for most areas of the United States have increased to $726,200 for single-family homes. This is an increase from the 2022 limit of $647,200.

What are Conforming Loan Limits?

Simply put, conforming loan limits are the maximum loan amounts that can be backed by government-sponsored entities (GSEs) like Fannie Mae and Freddie Mac. These entities purchase mortgages from lenders, allowing them to free up capital and make more loans.

When a mortgage conforms to the loan limits set by the GSEs, it is considered a conforming loan. These loans are seen as less risky for lenders because they are backed by the government, making them more accessible to borrowers.

How are Conforming Loan Limits Determined?

The Federal Housing Finance Agency (FHFA) sets the conforming loan limits each year based on the average home price in the previous year. The FHFA uses data from the Federal Housing Administration (FHA) to determine the average home price.

If the average home price increases from one year to the next, the conforming loan limits will also increase. This is to ensure that borrowers have access to affordable mortgage financing even as home prices rise.

What Do Conforming Loan Limits Mean for Borrowers?

If you are looking to obtain a mortgage, conforming loan limits can affect your ability to get a loan. Here are some ways it can impact borrowers:

- Loan Amounts: If you need to borrow more than the conforming loan limit in your area, you will have to look for a jumbo loan. These loans are not backed by the government and are considered riskier for lenders, making them more difficult to obtain.

- Interest Rates: Conforming loans typically have lower interest rates than jumbo loans because they are seen as less risky. This means you may be able to save money on your mortgage payments with a conforming loan.

- Down Payment: Because conforming loans are seen as less risky, lenders may require a lower down payment than they would for a jumbo loan. This can make it easier for borrowers to qualify for a loan.

How Does Conforming Loan Limit Apply to VA Loans?

For VA loans, the conforming loan limit does not apply in the same way as it does for conventional loans. VA loans are backed by the Department of Veterans Affairs (VA) and are not subject to the same loan limits as conventional loans.

Instead of conforming loan limits, VA loans have what is known as a “VA entitlement.” This entitlement is the amount of money the VA guarantees to the lender in the event that the borrower defaults on the loan. For most veterans, the VA entitlement is $36,000, but it can be higher for those who have served for longer periods of time or who have used their VA benefits before.

The VA does not set the loan limits for VA loans on a first home purchase. However, on a second home purchase, we would need to consider the county loan limit as well as the remaining entitlement to determine what you would qualify for without a downpayment.

It’s also worth noting that the VA does not limit the amount of money that a lender can lend to a borrower for a VA loan. Instead, the VA focuses on the amount of the loan that they will guarantee, which can make it easier for veterans to qualify for a mortgage.

FAQs:

Q: Do VA loans have lower interest rates than conventional loans?

A: VA loans typically have lower interest rates than conventional loans. Lenders see them as less of a risk. Factors such as credit score and down payment may affect the interest rate of your VA Loan.

Q: Can you purchase an investment property with a VA Loan?

A: No, VA loans can only be used to purchase primary residences.

Q: Is there a limit to how many times a veteran can use their VA entitlement?

A: No, there is no limit to how many times a veteran can use their VA entitlement as long as they have not defaulted on a previous VA loan.

Conclusion:

Conforming loan limits and VA loan entitlements are important factors to consider when applying for a mortgage. Knowing what they are and how they apply to your specific situation can help you make informed decisions about your home financing options.

For 2023, the conforming loan limits have increased to $726,200 for most areas of the United States. While VA loans are not subject to the same loan limits, they do have their own requirements for loan amounts and entitlements.

If you’re a veteran looking to purchase a home or refinance your current mortgage, a VA loan may be a good option for you. It’s important to consult with a lender like VLG to determine the best course of action based on your individual circumstances.